Global Valve & Actuator Market

Outlook likely to Brighten Further

Global GDP growth is estimated to have expanded 2.9%, slightly better than the 2.7% expected at the time of the report. Thus, the strong rebound in valve and actuator markets across most of the world in 2017 suggests that our bullish outlook may be upgraded further in the next report.

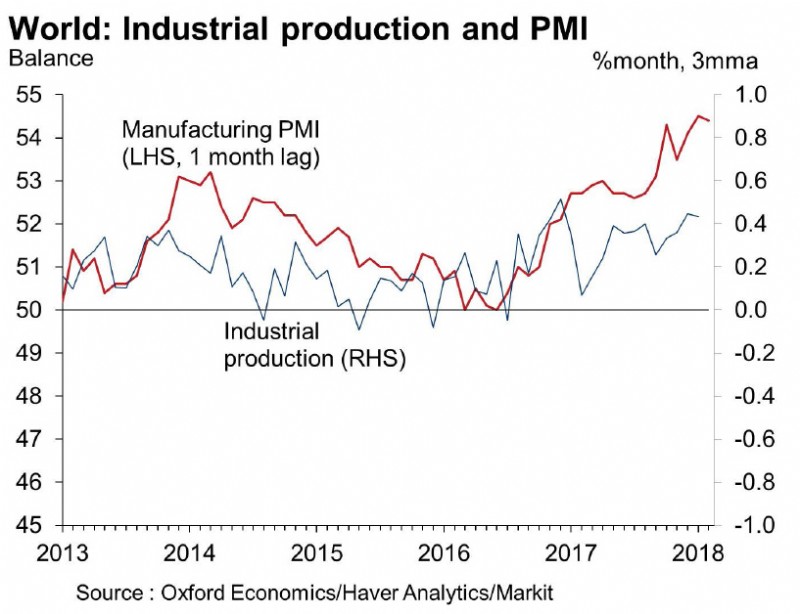

Strong global trade, recovery in commodity prices, weak US dollar and weaker than anticipated inflation along with improved credit conditions and tightening labor markets have been the key drivers behind this years global upturn. In December, the global composite PMI continued to trend upwards, rising to its highest level of 2017. Evidence that the global economy ended 2017 on a high note suggests that the underlying momentum of the world economy is being maintained and that the omens for 2018 are positive. So, we have upgraded our global GDP growth forecast for 2018 slightly from 3.0% to 3.2%.

World industrial production expanded at 3.5% in 2017, and early evidence strongly suggests it will exceed that pace this year, with much of the strength emanating from the developed world.

The fact that this growth is more rapid than for overall GDP signals a sustained industrial upcycle. Even in the UKwhere uncertainties around Brexit have put significant headwinds on industrial activity the broader rebound in global trade has led to a much stronger industrial outlook this year. Spare capacity is decreasing across the developed world, and this, combined with a solid investment rebound and robust demand is powering industrial activity, particularly in heavy manufacturing industries like base metals and mechanical engineering. Growth in consumer-facing sectors such as food & beverageswhich tend to be less cyclical than heavy manufacturingis expected to be resilient even amid a mild acceleration in inflation as tight labour markets begin to feed strong growth in incomes and spending power.

The breadth of the industrial upturn is particularly beneficial for the chemicals sector, whose products are used across the industrial spectrum. We expect well over 4% growth in production this year, let by a 6% increase in the US as large investments in new facilities there start coming onstream. The construction outlook is also robust, despite fears of supply side constraints in the US and reduced Chinese government support for the housing sector.

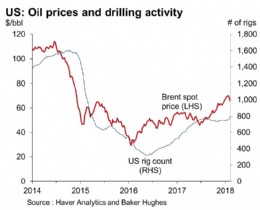

The oil and gas sector has also seen a reversal of fortune. Despite recent drops, oil prices are more than double their lows of 24 months ago which has sparked a renaissance in the US unconventional sector. After a market shakeout in 2016 that decimated activity, the number of rigs in operation has more than doubled in the US. The pickup in oil prices should be followed by an uplift in US oil investment, as rig counts tend to track the oil price with a lag of around 3-6 months. Indeed, we already see evidence of this as rig counts are up by almost 30% year-on-year in February 2018. On this basis, we are confident that US oil and gas investment will grow by more than 25% this year.

All of these developments point to a possible upgrade of this years valve and actuator market growth outlookparticularly in the developed world where demand has picked up the most. Last years expectation for 2.8% growth in the US for 2018 will be further supported by the fiscal stimulus package along with ongoing strength in global activity and the oil sector rebound. Even in Europewhich we boldly predicted would be the fastest-growing regions next year in terms of valve and actuator demandindustrial performance relative to our view in the previous report have exceeded expectations across all major countries, with Germany leading the way.

Jeremy Leonard and Noel Saraf are, respectively, Director of Global Industry Services and Senior Economist at Oxford Economics. The 2018 edition of the Global Valve and Actuator Market Outlook will be published at the end of March 2018.

Oxford Economics

Tel: +44 (0)203 910 8036

Published: 22nd March 2018

Rachel Wormald, Managing Director at YPS Valves Ltd and Elizabeth Waterman, ...

Are you looking for industry-leading, brand independent valve and actuator ...

As can be seen from the photograph, clearly the resident birds at Bartlett ...

Howco Group has unveiled its latest £1million investment, with the ...

In 2024, Allvalves is poised for an exciting year of growth and expansion, ...

GMM Pfaudler Engineered Plastics & Gaskets are delighted to bring the ...

In the ever-evolving valve industry, GMM Pfaudler stands out for its ...

SAMSON Controls Ltd – part of the SAMSON group - a renowned leader in ...